![]()

![]()

Despite your best efforts, chargebacks do sometimes happen. When a transaction is disputed, the chargeback process works as follows:

The card-holder (your customer) calls the bank that issued the credit card to dispute a charge.

The bank contacts your merchant processing provider and informs it of the disputed charge.

Your merchant processing provider makes an initial judgment as to the validity of the disputed charge. (It may request a copy of the receipt for the disputed charge before making a decision—see Retrieval Request Letter below.)

If your merchant processing provider decides the chargeback is valid it will:

Immediately debit your bank account for the amount of the transaction.

Assess a Chargeback Fee that will be debited from your bank account on the next scheduled transaction fee debit date. (This will vary based on the terms of your merchant processing contract.)

Send you a “Chargeback Debit Advice” letter (see Chargeback Debit Advice Letter below) along with any supporting documentation available, and a “Chargeback Adjustment Reversal Request” form that contains instructions on what you need to do to defend your business and have the Chargeback reversed. This will be sent via mail to your address of record on the same day that your bank account is debited-so you may see the debit before you receive the letter.

You (the merchant) decide whether to dispute the Chargeback.

If you

don't want to dispute it, do nothing. The issue will be considered

closed and the reversal of the charge will be permanent.

NOTE: Chargebacks in excess of 2%

of your total processing volume in any 30 day period are grounds

for suspension or termination of your merchant processing account.

If you want to dispute the Chargeback and have it reversed, complete and submit the "Chargeback Adjustment Reversal Request" form by the date indicated in the "Chargeback Debit Advice" letter. Make sure to include all information and documentation requested in the "Merchant Action Necessary to Remedy Chargeback" section of the form.

Your merchant processor reviews the information you provided, and makes a final decision on whether to reverse the Chargeback. (During this process it may contact the Card Issuer to attempt to collect payment for the charge based on the information you provide.)

You are informed of the final decision. If the chargeback is reversed, the amount of the transaction is credited back to your bank account.

|

If you do have a Chargeback please don't hesitate to call your service provider for assistance with gathering documentation and defending it. You can also call your merchant processor's customer service line for assistance. |

As part of the chargeback process, you will receive multiple communications from your merchant processing provider. The following are samples of the two most common letters:

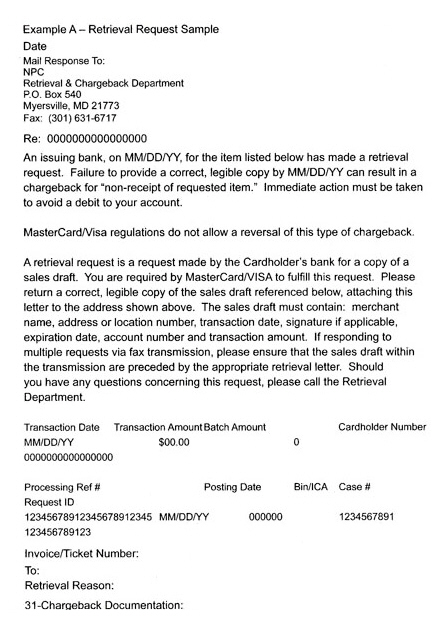

Merchants are required to maintain original authorization documents and transaction receipts for a period of two (2) years. A Cardholder is permitted to request a copy of sales or credit drafts within this time frame. This is known as a Retrieval Request.

Upon receipt of a Retrieval Request from a Cardholder bank, your merchant processor will mail a Retrieval Request Letter to your address of record. This form contains pertinent information of the original sale. A legible copy of the sales receipt and authorization must be faxed or mailed to the address or fax number indicated on the Retrieval Request Letter within five (5) days. It is important that you retain a copy of all submitted documents for your records. A sample letter is shown below:

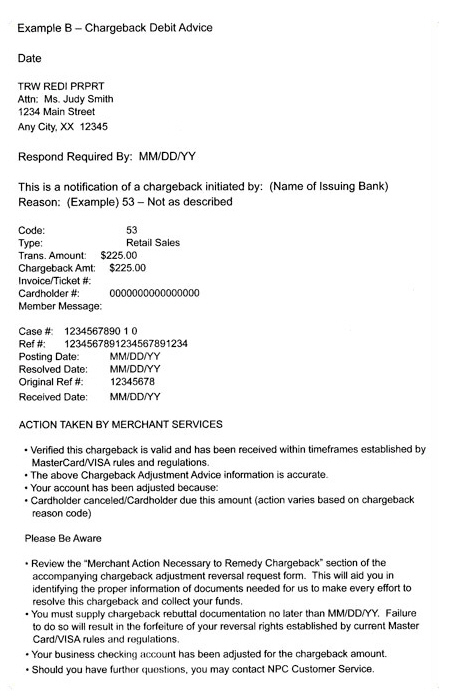

Chargeback Debit Advice Letter

When your merchant processor has initially validated a chargeback, this letter will be sent to your address of record. If you want to defend the chargeback and have it reversed, you must supply the information and documentation requested in the letter by the date indicated. A sample of a Chargeback Debit Advice letter is shown below:

Next Section: Authorizing Echeck (ACH) Transactions >